Decomposing Venture: Buyer Power

Global Investor Hannah Savage talks 'The Bargaining Power of Founders in VC'

Forces One and Two

First we covered Force One: The Threat of New Entrants: Why Everyone (Apparently) is a VC Now. Second we covered Force Two: The Bargaining Power of Suppliers (Limited Partners). This week we will continue to break down the venture capital industry with Force Three of Porter’s Five Forces.

Force Three

Third up: The Bargaining Power of Buyers (Founders).

As we continue our analysis of the venture capital industry, remember that Porter's Five Forces framework is a crucial tool for analyzing the competitive intensity and attractiveness of a market. A key force is the bargaining power of buyers, which examines the influence customers have on pricing and competition. The bargaining power of buyers in an industry significantly affects the competitive environment and influences the seller’s ability to achieve profitability. Strong buyer power enables buyers to pressure sellers to lower prices, demand higher quality and expect more and better services, which can reduce the seller's profitability. Conversely, when buyer power is low, it increases the profit potential of an industry, as sellers can dictate terms.

It’s important to acknowledge that founders are not traditional “buyers” and actually are “sellers” of an asset: equity in a company. However, for the purpose of this analysis, we will refer to founders as “buyers” because they are “acquiring” and “consuming” the product, capital, of a VC firm. Analyzing through this lens can give us a better understanding of the dynamics between founders and investors.

Let’s look at the factors that determine high or low bargaining power of founders.

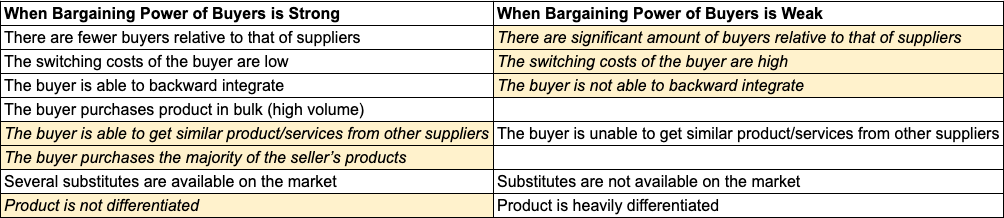

Buyers Relative to Suppliers

When buyer power is strong: There are fewer buyers relative to suppliers.

When buyer power is weak: There are a significant number of buyers relative to suppliers.

Founder's situation:

There are far more startups seeking funding than there are VC funds available.

This dynamic favors VC firms, especially the more prestigious ones. They can be highly selective, leading to less bargaining power for the majority of founders.

Founders, particularly those at early stages, often face a scarcity of funding options, limiting their ability to negotiate favorable terms.

Switching Costs

When buyer power is strong: The switching costs of the buyer are low.

When buyer power is weak: The switching costs of the buyer are high.

Founder's situation:

Securing funding is a time-consuming and arduous process for founders.

Building relationships with VCs, pitching, due diligence and negotiating term sheets all demand significant effort.

If a deal falls through, founders must often start the process over, incurring substantial "switching costs" in terms of lost time and momentum.

This time constraint and the urgent need for capital can force founders to accept less-than-ideal terms, reducing their bargaining power.

Backward Integration

When buyer power is strong: The buyer is able to backward integrate.

When buyer power is weak: The buyer is not able to backward integrate.

Founder's situation:

"Backward integration" in this context would mean founders gaining direct access to the sources of capital that supply VC firms (limited partners or LPs).

While some very successful founders eventually become VCs themselves, this is not a viable option for most startups.

Founders generally lack the resources, connections and track record to raise capital directly from LPs.

This dependence on VC firms as intermediaries strengthens the VCs' position.

Purchase Volume

When buyer power is strong: The buyer purchases product in bulk (high volume).

When buyer power is weak: The buyer is limited in their purchasing power.

Founder's situation:

Startups often require funding in stages from multiple VC firms.

They typically cannot raise all the capital they need from a single source, especially as they grow.

This need to "purchase" capital from several "suppliers" (VCs) can fragment the founder's bargaining power. Each VC has leverage related to their portion of the funding.

Product/Service Similarity

When buyer power is strong: The buyer is able to get similar products/services from other suppliers.

When buyer power is weak: The buyer is unable to get similar products/services from other suppliers.

Founder's situation:

While "capital is capital" in its basic form, VC firms try to differentiate themselves.

Some VCs offer valuable extras like mentorship, networking, branding and operational support.

If a founder highly values these extras, they may be willing to concede on other terms, increasing the VC's bargaining power.

However, if founders perceive capital as largely undifferentiated, they may focus more on financial terms (valuation, etc.).

Proportion of Product Purchased

When buyer power is strong: The buyer purchases the majority of the seller’s products.

When buyer power is weak: The buyer purchases a small subset of the seller’s products.

Founder's situation:

VC firms primarily "sell" capital as their core "product."

Startups, especially those in early stages, are heavily reliant on this specific product.

This reliance increases the VC's power, as the startup has few alternative customers for the VC's capital.

Availability of Substitutes

When buyer power is strong: Several substitutes are available on the market.

When buyer power is weak: Substitutes are not available on the market.

Founder's situation:

Founders have access to various VC firms, but the type of capital available is often similar (equity financing).

Alternative funding sources, such as bank loans, are often more difficult for startups to obtain, especially in early stages.

This limited availability of substitute funding options can increase the bargaining power of VCs.

Product Differentiation

When buyer power is strong: Product is not differentiated.

When buyer power is weak: Product is heavily differentiated.

Founder's situation:

As mentioned, capital itself is largely undifferentiated.

This can make founders more sensitive to other deal terms, such as valuation and control, as the core "product" is essentially the same across different VC firms.

The power dynamic between venture capital (VC) firms and founders is a significant consideration within the industry. It is widely acknowledged that a power imbalance exists in this relationship. From Porter’s perspective, this imbalance could be seen as a factor contributing to the attractiveness of VC investment, as firms possess considerable influence in negotiating terms and allocating capital.

Terms and Control: VCs Exercise Power

Terms:

Valuation: Higher valuations mean founders give up less equity, preserving their ownership and control. VCs with more power can often negotiate lower valuations.

Equity: VCs negotiate the percentage of equity they receive for their investment as founders become diluted in their equity stake.

Liquidation preference: Higher liquidation preferences favor VCs, who get paid back first (and often multiple times their investment) before common stockholders (founders, employees). This can create a situation where founders get little to nothing even if the company has a decent exit.

Participation rights: Allows VCs to get their liquidation preference and participate in the remaining proceeds as if they were common stockholders. This significantly increases the VC's upside and reduces the founder's share.

Control:

Board seats: VCs often require a seat on the company's board of directors. Board members have significant influence over strategic decisions, hiring/firing and major transactions. More board seats for VCs mean less control for founders.

Voting rights: Determines who gets to vote on key company decisions. VCs may negotiate for preferred stock with special voting rights that give them more power than common stockholders.

Protective provisions (veto rights): VCs may demand veto rights over certain company actions, such as:

Selling the company

Raising more debt or equity

Changing the company's bylaws

Major expenditures

However, the potential consequences of excessive power warrant examination.

Founder Leverage

Not all founders are completely at the mercy of their investors. Some founders do have significant bargaining power.

Serial entrepreneurs with successful exits

Startups in hot sectors with high growth and strong metrics

Founders with unique expertise or technology

Conclusion

The analysis reveals a clear power imbalance between VC firms and founders. This imbalance, while potentially contributing to the attractiveness of VC investment by enabling firms to negotiate favorable terms, has led to increased scrutiny from founders who are advocating for more equitable treatment. This power dynamic is evident in the terms of VC deals, where factors like valuation, liquidation preferences and anti-dilution provisions can significantly impact founders' ownership and financial returns. Furthermore, control mechanisms such as board seats, voting rights and protective provisions enable VCs to influence company strategy and operations, sometimes limiting founder autonomy.

However, it’s important to note that founder leverage exists, particularly for serial entrepreneurs, high-growth startups and those with unique expertise. Evolving market conditions and increased founder awareness are driving a demand for change, with some investors adopting more founder-centric approaches. Addressing the power imbalance is crucial for the long-term health and sustainability of the VC ecosystem.

This series will continue with Force Four: Threat of Substitutes (Bank Loans, Crowdfunding, etc.).

Sources

STRATEGIC CFO: Buyer Bargaining Power (one of Porter’s Five Forces)

Paul Hastings: Navigating Control Mechanisms in Startups

Feld, Brad, and Jason Mendelson. Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist. 4th ed., Wiley, 2019.

Subscribe

Follow the “Decomposing Venture” series by Global Investor Hannah Savage using the “Subscribe now” button below.

| A guest post by

|